Labor and Employment Alert: A Flurry of Employee Benefit Guidance in the Closing Days of the Obama Administration

2015 Pay or Play Penalties

According to IRS FAQs on IRC §4980H published December 22, 2016, the IRS will begin contacting employers in “early 2017” regarding potential liability for 2015 pay or play penalties under IRC §4980H. A letter from the IRS will be a notice of potential liability, not an assessment of liability; an employer will have an opportunity to respond prior to an assessment. The IRS expects to publish guidance on the process before the letters go out to employers. The IRS also expects to contact employers that the IRS suspects may be applicable large employers (i.e., employers with 50 or more full-time plus full-time equivalent employees in 2014) that failed to file Form 1095-Cs for 2015. If you get either of these types of letters from the IRS, we can assist with an analysis of your data and the response to the IRS.

2016 Treatment of Opt-Out Payments

An opt-out payment is an amount that an employer pays an employee if and only if the employee waives the employer’s medical plan. For example, assume an employee would need to make a salary reduction contribution of $200 per month to enroll in the employer’s medical plan and the employer would pay the employee $100 per month if the employee waives the medical plan. What is the employee contribution in this example? The answer depends on why the question is being asked.

- Premium assistance: When an employee applies for premium assistance to purchase individual health insurance through the Marketplace, the Marketplace is supposed to determine whether the employee is eligible for “affordable” medical coverage from his or her employer. The employee is eligible for “affordable” medical coverage from his or her employer if the required contribution for single coverage does not exceed the applicable percentage of the employee’s household income (9.69% for 2017). For this purpose, the Marketplace considers the employee’s required contribution to be $300 per month, consisting of the $200 salary reduction contribution plus the $100 the employee would give up if he or she enrolled in the employer’s medical coverage. The IRS “encourages” (but does not require) employers to provide information to employees on the treatment of opt-out payments for purposes of an employee’s eligibility for premium assistance.

- IRC §4980H(b) unaffordable/inadequate coverage penalty: In contrast, an employer may report the required contribution (Form 1095-C Line 15) as $200 (ignoring the $100 opt-out payment) for 2016, provided that the opt-out arrangement has been in effect since December 16, 2015. (If the opt-out arrangement was implemented after December 16, 2015, the employer would have to report the required employee contribution as $300, including the $100 opt-out payment.) The amount reported on Form 1095-C Line 15 is used to determine an employer’s potential liability for the unaffordable/inadequate coverage penalty under IRC §4980H(b).

The answer may be different for 2017. The IRS currently expects to issue regulations requiring the inclusion of unconditional opt-out payments in the required contribution for purposes of the IRC §4980H(b) unaffordable/inadequate coverage penalty, to match the treatment of opt-out payments for purposes of premium assistance. However, the new Administration may choose different treatment – or Congress could repeal the pay or play penalties or change them in a way that makes the question irrelevant.

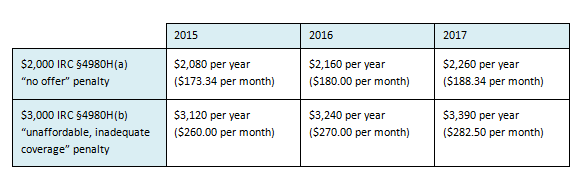

2017 Indexed Pay or Play Penalties

The IRS indexed the employer pay or play penalties. The 2017 amounts will apply to failures to offer affordable, minimum value health coverage to full time employees in 2017 – unless changed or repealed by Congress.

Other group health plan indexed amounts are on this chart.

2018 Claims and Appeals Process for Disability Benefits

On December 19, 2016, the Department of Labor published final regulations on claims and appeals for disability benefits. The regulations will be effective for claims filed on or after January 1, 2018 – unless Congress chooses to disapprove the regulations. The regulations are not related to the Affordable Care Act, so are not necessarily in the crosshairs of the new Administration. Nonetheless, Congress has the power to block these and other regulations published after May 30, 2016.

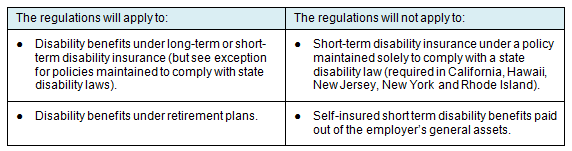

If the regulations go into effect as scheduled, they will apply to most but not all claims for disability benefits.

The new regulations would:

- increase the amount of information that must be provided to a claimant during the claims and appeals process, including:

- a copy of any specific internal rule, guideline protocol, standard or other criteria relied upon in making an adverse benefit decision;

- documentation of the reasons for any disagreement with the treating physician;

- if the plan considers a new reason for an adverse benefit decision, require disclosure of that reason and provide a reasonable opportunity for the claimant to respond; and

- require language assistance for non-English speaking claimants under some circumstances; and

- prohibit a plan from considering the likelihood of a service provider denying a claim as part of any hiring, compensation, promotion, termination or similar review of a service provider.