Claiming Federal Relief Tax Credits and Deferring Payroll Tax Payments

Recent Federal COVID-19 legislation provides employers with a number of new potential tax credits. The FFCRA (Phase II relief) requires certain employers to provide COVID-19 related sick-leave and FMLA leave on or after April 1, 2020, while at the same time providing a refundable tax credit to most such employers for wages required to be paid under these new mandates (the Qualified Leave Credit). The Qualifying Leave Credits are described in further detail in Vorys’ March 19 Client Alert: The Families First Coronavirus Response Act: What Employers Need to Know. The CARES Act (Phase III relief) provides certain employers with the ability to claim a refundable tax credit for qualifying wages paid during periods of partial or complete shutdown, or significant decline in gross receipts, resulting from COVID-19 (the Employee Retention Credit). The Employee Retention Credits are described in further detail in Vorys’ March 28 Client Alert: The CARES Act Impact on Employee Benefit Plans. In addition, the CARES Act permits a delay in payment of the social security portion of an employer’s payroll tax liability on employee salaries (Employer Social Security Tax) for the period beginning March 27, 2020 and ending on December 31, 2020, as discussed further in Vorys’ March 27 Federal Tax Bulletin: CARES Act Extends Deadline for Payment of 2020 Employer and Self-Employment Social Security Tax.

Since enactment of the FFCRA and the CARES Act, the Treasury Department and IRS have released piecemeal guidance on claiming the Qualified Leave Credit and the Employee Retention Credit, as well as deferring payroll tax payments. Pursuant to this guidance, employers are able to accelerate access to cash by reducing overall payroll tax deposits by the amount of accrued Qualified Leave Credits and Employee Retention Credits. The IRS has indicated, however, that any Employee Retention Credits accrued in the first calendar quarter of 2020 (related to qualifying wages paid between March 13, 2020 and March 31, 2020) may not be reported on an employer’s first quarter payroll tax return (typically a Form 941), but rather must be reported on an employer’s second quarter Form 941. How this rule impacts an employer’s ability to use accrued Employee Retention Credits to offset first quarter payroll tax deposits is not entirely clear (as discussed further below). As with all aspects of Federal COVID-19 relief, guidance on claiming federal tax credits and deferring payroll tax liability is rapidly evolving and is subject to change. The following provides an outline of guidance on these issues as of the date of this alert.

Deferral of Payroll Tax Deposits. The IRS has indicated that employers are entitled to defer deposits and payments of Employer Social Security Tax “that would otherwise be required to be made” during the period beginning on March 27, 2020 and ending on December 31, 2020 (the Deferral Period). Therefore, under this guidance, a payment or deposit due within the Deferral Period that relates to wages accrued prior to the Deferral Period would be eligible for deferral, while a payment or deposit due in January 2021 that relates to 2020 wages would not be eligible for deferral.

Although the first quarter 2020 Form 941 has not been modified to provide for the possibility of deferral of Employer Social Security Tax, the IRS has confirmed that employers were eligible to defer such payments and deposits beginning on March 27, 2020. The IRS will provide information in the “near future” to instruct employers how to report deferrals for the first quarter of 2020. No special election is required to defer Employer Social Security Tax.

Employers who have a Paycheck Protection Program (PPP) loan forgiven under the CARES Act may not also defer Employer Social Security Tax. However, the IRS has clarified that employers who obtain a PPP loan are still entitled to defer payments and deposits of Employer Social Security Tax that are required to be made through the date the lender issues a decision to forgive the loan, but the employer may not defer deposits and payments required to be made after such date. Amounts deferred by an employer on or before the date any portion of the PPP loan is forgiven may continue to be deferred through the generally applicable extended payment deadlines.

Claiming Qualified Leave Credits and Employee Retention Credits. Employers have three different methods to claim Qualified Leave Credits and Employee Retention Credits:

- Reduction of Payroll Tax Deposits. Each of the Qualified Leave Credit and the Employee Retention Credit generally is described in its authorizing legislation as a refundable credit against an employer’s social security tax liability (which is a component of an employer’s overall payroll tax liability equal to 6.2% of wages, subject to a cap). Nevertheless, Treasury has indicated that employers who accrue Qualified Leave Credits and/or Employee Retention Credits during a calendar quarter can reduce their overall payroll tax deposits for all employees for that quarter (including withheld federal income tax, the employee’s share of social security and Medicare, and the employer’s share of social security and Medicare) by the amount of the accrued credit. In fact, this practice is encouraged in the instructions to Form 7200, which state that employers “should retain an amount of the payroll taxes equal to the [credits] rather than depositing these amounts with the IRS.” This provides employers with the quickest possible access to cash resulting from the credit. Any reduction in deposits resulting from the credits will be reported on the employer’s next Form 941.

- Refund of Excess Credits. In the event that an employer ends up with a greater credit amount than their reduction in payroll tax deposits, the employer is entitled to claim a refund for the excess credit amount on their Form 941 for that quarter, unless they have already claimed an advance refund, as described below.

- Advance Refund. Employers are not required to wait until they file their Form 941 to claim a refund relating to Qualified Leave Credits or Employee Retention Credits. At any point during a calendar quarter during which an employer is accruing Qualified Leave Credits and/or Employee Retention Credits, if the employer has accrued credits at that point in excess of reductions the employer has made in payroll tax deposits for that quarter, the employer can file Form 7200 claiming an advance refund in the amount of the excess. An employer is entitled to file multiple Forms 7200 with respect to a single quarter, through the end of month following the quarter end. This again reflects efforts by Treasury and the IRS to facilitate employer quick access to cash to continue funding payroll.

Coordination with Payroll Tax Deferral. Some employers will be entitled to defer Employer Social Security Tax until after 2020 (as discussed above), and also to claim Qualified Leave Credits and/or Employee Retention Credits. The IRS has indicated that, in such event, an employer is entitled to first defer Employer Social Security Tax payments. The employer is then entitled to offset any accrued credits against the non-deferred deposit amount, and to obtain a refund for any excess credits. In other words, under this guidance, an employer’s deferral of Employer Social Security Tax will not reduce its ability to claim Qualified Leave Credits or Employee Retention Credits.

First Quarter Employee Retention Credits. Employee Retention Credits are potentially available for first quarter 2020 wages. (Qualified Leave Credits are only available for qualifying wages paid on or after April 1.) Generally, current guidance requires that Qualified Leave Credits and Employee Retention Credits accrued in a quarter be claimed, at the latest, on the Form 941 filed with respect to such quarter. However, the IRS has released a special rule for first quarter Employee Retention Credits. An employer entitled to Employee Retention Credits for first quarter 2020 is not to report those credits on their first quarter Form 941, but rather is to report those credits, along with credits accrued during the second quarter, on the employer’s second quarter Form 941. This requirement creates uncertainty as to whether Employee Retention Credits accrued during the first quarter may reduce first quarter payroll tax deposits, or whether the credits may be used only to reduce second quarter payroll tax deposits. Perhaps the IRS will provide additional guidance on this question in connection with anticipated guidance on reporting of first quarter payroll tax deferral (discussed above). If not, although not entirely clear, based on the existing guidance from Treasury and IRS to date it appears that employers will not incur a penalty for the first quarter as a result of reducing deposits by accrued Employee Retention Credits (even though the first quarter Form 941 would then show an underpayment of payroll tax). In this case, an employer should attach a statement to their second quarter Form 941 explaining the first quarter underpayment and adjusting the second quarter offsets accordingly. Alternatively, an employer that has reduced first quarter payroll tax deposits could (i) make additional deposits to offset the earlier reductions prior to filing the first quarter Form 941, and (ii) reduce their second quarter payroll tax deposits by the same amount.

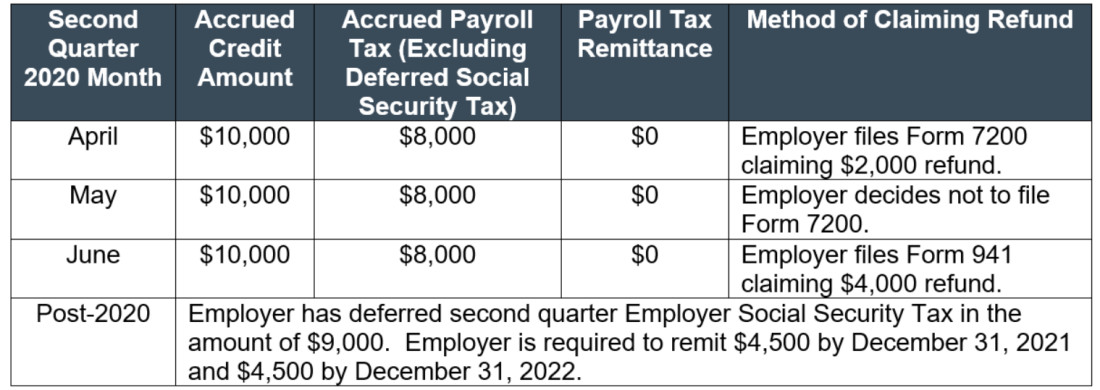

Example. The following example illustrates the operation of a number of the rules discussed above. For purposes of this example, assume the following:

- A calendar-year employer files Form 941, and makes monthly payroll tax deposits that would normally equal $11,000 per month.

- The employer elects to defer all Employer Social Security Tax payments and deposits until after 2020, which is an amount equal to $3,000 per month in second quarter 2020.

- The employer’s required payroll tax deposit amount for income tax withholding, the employee’s share of Social Security tax and both the employer’s and employee’s shares of Medicare taxes in second quarter 2020 is $8,000 per month.

- The employer accrues $10,000 of Employee Retention Credits monthly during second quarter 2020.

As Treasury and the IRS continue to consider all aspects Federal COVID-19 relief, guidance on all issues continues to evolve. Employers considering claiming Qualified Leave Credits and/or Employee Retention Credits should be certain to stay abreast of current developments.

Contact your Vorys attorney with any questions.

--

VORYS COVID-19 TASK FORCE

Vorys attorneys and professionals are counseling our clients in the myriad issues related to the coronavirus (COVID-19) outbreak. We have also established a comprehensive Coronavirus Task Force, which includes attorneys with deep experience in the niche disciplines that we have been and expect to continue receiving questions regarding coronavirus. Learn more and see the latest updates from the task force at vorys.com/coronavirus.