Labor and Employment Alert: No Auto-Enrollment into Health Plans and Other Employee Benefit News

No auto-enrollment into health plans

The Bipartisan Budget Act of 2015 (11/2/2015) includes a rare bipartisan amendment to the Affordable Care Act (ACA). The ACA would have required that employers with 200 or more full-time employees auto-enroll their full-time employees in health coverage. The requirement did not have a specific effective date, and the DOL had suspended the requirement indefinitely while it puzzled over how auto-enrollment could be accomplished without defaulting employees into health coverage (and payroll deductions) they did not want. Now, auto-enrollment is permanently off the agenda.

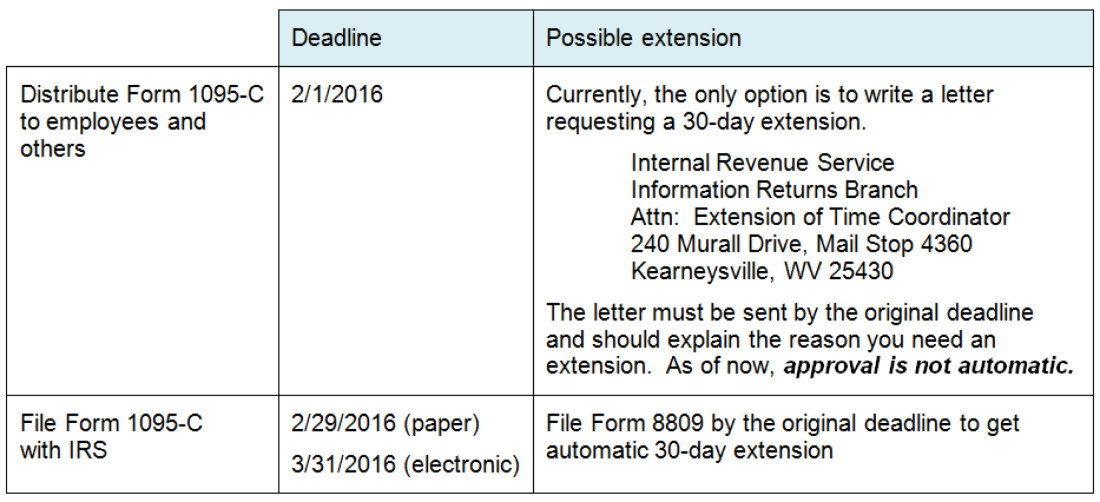

Are you ready for Form 1095-Cs?

Approaching deadlines

If your company is an “applicable large employer” (generally, 50 or more full-time and full-time equivalent employees), you have probably made arrangements for completing, distributing, and filing Form 1095-Cs. If not, you will want to prioritize that project. Deadlines are approaching.

Who gets a Form 1095-C?

The IRS will use the information on Form 1095-Cs to:

- Determine an employer’s liability for pay or play penalties;

- Determine whether an individual is entitled to federal subsidies for the purchase of individual health insurance through a public Marketplace; and

- Enforce the individual mandate.

Because the purpose of the Form 1095-C is not limited to determining an employer’s liability for pay or play penalties, recipients are not limited to an employer’s full-time employees. If your company is an “applicable large employer” with a self-insured health plan, you have to provide a Form 1095-C to:

- Every individual who met the IRS definition of a “full-time employee” in one or more months (regardless of whether they were offered or enrolled in coverage under your health plan); plus

- Every other individual (e.g., a part-time employee, former employee, partner, or former spouse) who was enrolled in your health plan other than as a dependent of another person. Dependents are listed on the Form 1095-C provided to the person (e.g., employee, former employee, or partner) through whom the dependents were enrolled.

See this flowchart for details.

Notices

If the IRS sends you a notice regarding a Form 1095-C, you will want to respond in order to avoid inaccurate assessment of pay or play penalties. However, a notice from the IRS regarding a Form 1095-C should not be confused with a notice from the Department of Health and Human Services (HHS). Starting next year, HHS will be phasing in a notice process that will be triggered when an individual: (a) applies for federal subsidies for the purchase of individual health insurance in a federally-run Marketplace (like Ohio’s Marketplace) and (b) identifies you as his or her employer. HHS will notify you of your company’s potential liability for pay or play penalties and will provide an option to appeal. However, an appeal of an HHS notice just gives you the opportunity to dispute the accuracy of some of the information in the individual’s application for federal subsidies. This may result in the cancellation of advance payment of federal subsidies. However, an appeal of the HHS notice will not preclude a separate notice from the IRS (or the IRS’ assessment of pay or play penalties) based on information the IRS gleans, after year-end, from the individual’s Form 1095-C and tax return.

The DOL Marketplace Notice is intended to help employees understand who is and who is not eligible for their employer’s health coverage and whether that coverage meets minimum value and affordability standards. You are supposed to give a copy of the Marketplace Notice to new hires but you may also want to post an updated version of the Marketplace Notice on your company’s website for easy reference by any employees who might be wondering whether they would qualify for federal subsidies for the purchase of individual health insurance through a public Marketplace.

EEOC’s proposal regarding GINA and spousal health risk assessments

We know that you and your spouse are not genetically related. However, the Genetic Information Nondiscrimination Act (GINA) defines “genetic information” to include information about a family member’s health and further defines a “family member” to include your spouse. So, for purposes of GINA, information about your spouse’s health is treated as your genetic information. Why does this semantic oddity matter? GINA generally prohibits an employer from:

- Asking for genetic information before an individual is enrolled in health coverage; and

- Offering an incentive for the provision of genetic information, even after the enrollment in health coverage.

EEOC has proposed regulations that would provide an exception to the second prohibition (subject to certain conditions and limits), but not the first prohibition. If finalized as proposed, a spouse could not be asked to complete a health risk assessment before enrolling in health coverage. After enrolling in health coverage, however, a spouse could be asked to complete a health risk assessment and the employee could receive a financial reward for his or her spouse’s completion of a health risk assessment provided that:

- The reward does not exceed 30% of the incremental cost of family or spousal coverage. For example, if employee coverage costs $6,000 and family coverage costs $14,000, the reward for completion of the spousal health risk assessment could not exceed $2,400 (30% [$14,000 - $6,000]). Further, the 30% would serve as an overall limit on all wellness programs rewards including those not implicating GINA.

Comment: In April, the EEOC had proposed regulations on the application of the Americans with Disabilities Act (ADA) to wellness programs (summarized in our April 23, 2015 Client Alert). The EEOC’s proposed ADA regulations limited rewards to 30% of the cost of single coverage and did not address spousal participation.

- The spouse signs an authorization form describing how the employer will protect the collected information.

The IRS and DOL interpret the application of GINA to wellness programs that are part of a health plan, and the EEOC interprets the application of GINA to wellness programs that are employment policies (i.e., not part of a health plan). However, the EEOC has been coordinating with the IRS and DOL with respect to wellness programs so the EEOC’s proposed regulations may reflect the IRS and DOL position with respect to spousal health risk assessments.