Virtual Board Meetings And Risk Mitigation During COVID-19

Having addressed how to conduct hybrid or virtual-only shareholder meetings, corporate boards now must consider virtual board meetings in this COVID-19 era, and decide how to mitigate the additional legal risks they present.

This alert considers three key questions concerning virtual board meetings in the COVID-19 world: 1) are they allowed; 2) how best to manage them; and 3) how to mitigate the additional risks posed by them.

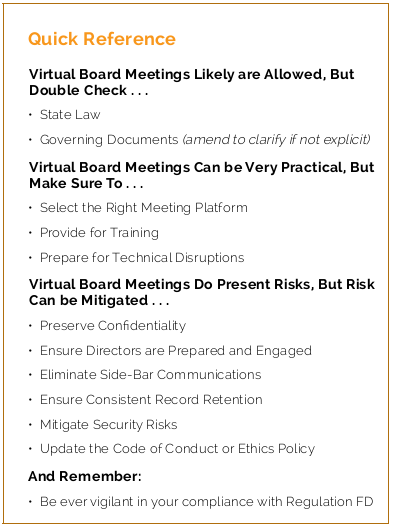

1) Virtual Board Meetings Likely are Allowed, But Double Check ...

State Law in the Corporation’s State of Incorporation. Most states permit virtual board meetings as long as board members are able to hear one another and the charter documents do not prohibit the format. See, e.g., Delaware Corporate Law Sec. 141(i).

Governing Documents, Including Corporate Charters, Bylaws, and Other Governance Documents. To remove all doubt about the permissibility of virtual meetings, boards should consider explicitly authorizing virtual meetings if corporate governance documents are silent or ambiguous.

2) Virtual Board Meetings Can be Very Practical, But Make Sure To ...

Select the Right Meeting Platform. Many platforms facilitate virtual meetings (though many are at capacity already this annual meeting season). Companies should focus on security, reliability, and usability. Experts recommend enterprise grade software over consumer grade for a more complete set of security features and control over document distribution and retention.

Provide for Training. Companies (utilizing their IT teams or software vendors) should provide advance training to board members on security and other key features. In addition, an IT professional should be on standby during meetings. It can be difficult to navigate technical issues while in a virtual meeting.

Prepare for Technical Disruptions. Have a backup plan for technical interruptions, such as to switch to a different platform or telephone if necessary or hold the meeting on a backup date or time.

3) Virtual Board Meetings Do Present Risks, But Risk Can be Mitigated ...

Preserve Confidentiality. To discharge their duty of loyalty (and perhaps duty of care) directors must maintain confidentiality. As the Delaware Court of Chancery recognized in Disney v. The Walt Disney Company, the “preliminary deliberations of a corporate board of directors generally are non-public and should enjoy a reasonable expectation that they will remain private.” Given that boards routinely consider and address significant amounts of non-public, material information, this requirement poses even greater challenges in virtual meetings where directors are working with electronic information.

Ensure Directors are Prepared and Engaged. The duty of care requires that directors have sufficient information, devote adequate time and attention to reviewing it, be engaged, and deliberate. These obligations can be more difficult in a virtual setting. Electronic media leaves indelible trails that can reveal a director’s diligence or lack thereof. Multi-tasking board members – e.g., texting, e-mailing or web surfing during a meeting – may be challenged later for insufficient care. Directors must be strongly cautioned on these risks and undertake to remain fully engaged.

Eliminate Side-Bar Communications. Directors can subject themselves and the company to broad discovery by using personal media (e.g., texting, instant messaging, or email) to discuss material corporate topics with each other. In KT4 Partners v. Palantir Tech. Inc., a books and records litigation, the Delaware Supreme Court ordered the inspection of personal emails and text messages of a public company’s directors and officers. These same risks are present in general litigation as well. To mitigate the risk, the company should: (i) ensure that directors and officers communicate about company matters only on company communication platforms, (ii) maintain company policies confirming that company business is not to be conducted on personal platforms, (iii) for virtual meetings, disable the instant messaging and equivalent features of the meeting platform, and (iv) stress that directors and officers must put personal devices aside during meetings.

Ensure Consistent Record Retention. If pre-meeting materials are physically delivered to participants, include a self-addressed envelope for their return to reduce the risk of disclosure of confidential materials. If materials are distributed electronically, use a medium that allows for control per the record retention policy (e.g., distribute the materials through an enterprise platform and work with IT to ensure compliance with the company’s retention program). If handwritten notes are discouraged during in-person meetings or gathered afterwards, establish a system to do the same for virtual meetings.

Mitigate Security Risks, Including Through the Use of Virtual Waiting Rooms, Ejecting Capabilities, and Passwords. Select a platform with enhanced security features and train a host to use them, including on how to (i) place participants in a virtual “waiting room” until the host allows them to join the meeting; (ii) use ejecting capabilities so that unauthorized participants can be removed; and (iii) use passwords to restrict access to the meeting. Security features such as these help mitigate risks of so-called “zoom bombing” and other unauthorized attempts to enter a confidential meeting, helping to ensure confidentiality. Consider also security features on certain platforms that allow the host to disable instant messaging capability, which helps eliminate the problem of side-bar communications.

Update the Code of Conduct or Ethics Policy. Company policies should prohibit the use of personal devices and media to communicate about material corporate topics. Given this new era of virtual board meetings, boards should review and update these policies as appropriate.

And Remember

Compliance with Regulation FD remains essential. The SEC specifically reminded companies to ensure they disseminate material COVID-19 related information broadly and to avoid selective disclosures. Given that fast-evolving, material issues may be discussed at upcoming board and management meetings, an unwary senior official could inadvertently violate Regulation FD by selectively disclosing material information to a subset of key constituents.

Stay tuned for further guidance in the coming weeks on issues confronting corporate boards in the COVID-19 era, including board oversight in crisis situations, board and management continuity, compensation considerations, and activist preparedness.

--

Vorys COVID-19 Task Force

Vorys is continuing to monitor the COVID-19 outbreak and related guidance to Insurers. In addition, Vorys attorneys and professionals are counseling our clients on a myriad of others issues related to the outbreak. We have established a comprehensive COVID-19 Task Force, which includes attorneys with deep experience in the niche disciplines that we have been and expect to continue receiving questions regarding coronavirus. Learn more and see the latest updates from the task force at vorys.com/coronavirus.