Comparative Economic Impacts of Data Centers and Manufacturing Centers in Ohio

This article originally appeared in the December 2025 edition of Development Incentives Quarterly.

By: Chris Magill, Vista Site Selection

As a certified economist regularly assessing the economic impact value of various land uses around the country, one of the questions I commonly get from governments is “what is the ROI of a data center?” What I’m not getting directly asked, but what I believe to be the question behind the question, is “should I give my key industrial site to a data center or wait for a manufacturer?”

As we know, governments and more specifically, economic developers, sometimes believe they have a duty to their communities to fill available development sites with the “highest and best” use. Every real estate decision comes with an opportunity cost. For years, we have had a general idea of the ROI brought forth by a manufacturer, which is that manufacturers create jobs, purchase machinery, and participate in a supply chain ecosystem both upstream and downstream.

Unlike manufacturing, data centers don’t carry the same widespread institutional knowledge from real estate and economic development professionals. The first manufacturing plant was built in 1790, and the first data center was built in 1945, however it wasn’t until the 2000s when data center facilities started to take form resembling what they are today. Over this time what has emerged as a universal perception about data centers is that they employ less direct jobs than a typical manufacturer and consume a lot more power than a typical manufacturer. While governments and policymakers have worked hard to educate themselves on data centers, the frequency of questions about data center ROI suggests more work can be done in articulating the economic impacts of data centers. This article will summarize an economic impact study authored by myself and my colleague Dr. James Maples at Vista Site Selection, to not only illustrate the economic impacts of a typical data center, but to provide proper context by comparing it to economic impacts of a typical manufacturing facility.

The study we authored performs a comparative analysis of the economic and fiscal contributions of two hypothetical projects in Ohio: a 250,000 sq. ft. data center and a 250,000 sq. ft. manufacturing facility. The findings underscore the strategic importance of data center investments in generating higher economic output, tax revenues, and sectoral diversification, while manufacturing facilities offer sustained employment benefits. It is worth noting however that “manufacturing” is not a specific industry but rather a sector. Certain manufacturing operations will carry a higher economic impact than a typical data center, however, when averaging all industries within the manufacturing sector, a typical data center will have higher marks.

The study was conducted using IMPLAN input-output modeling, a widely recognized methodology for assessing economic ripple effects across industries. The analysis incorporates construction, machinery, and labor expenditures over defined time horizons to estimate direct, indirect, and induced impacts on Ohio’s economy. In order to compare the two uses, we created a “typical” data center and manufacturing plant to model.

What is a “Typical” Data Center and Manufacturing Plant?

Data for both hypothetical studies are from real cases previously analyzed by Vista Site Selection. To support comparison of like cases, data were adjusted to expenditures per square foot by year. Next, expenditures were adjusted to model a hypothetical 250,000 square foot data center and a hypothetical 250,000 square foot manufacturing center. Three buckets were used in the analysis: construction (creating the facility), machinery and equipment (capital expenditures of equipment needed for operations to begin), and labor (operational costs of employees). Construction was modeled as a one-time cost over five years, machinery is modeled over ten years, and labor costs are listed as annual spending based on job estimates of 250 manufacturing workers and 80 data center workers.

Additional adjustments were made to support a “generalizable” comparison of the two hypothetical cases. Below were the two most notable adjustments.

- Manufacturing was analyzed using aggregated IMPLAN categories. Typically, IMPLAN uses 528 disaggregated industries which includes over 300 kinds of manufacturing industries. Using aggregated industries creates a single industry representing manufacturing which broadly describes manufacturing in general. Note that future analyses can quickly and easily be conducted to provide detailed examples of a specific kind of manufacturing.

- Data Centers Consume More Energy. For data center models, spending patterns in IMPLAN were adjusted to increase energy spending patterns to 40% for operations.

What were the results?

|

Metric (includes spinoff effects) |

Data Center | Manufacturing |

| All Jobs Created/Supported (includes construction) | 9,691 | 3,712 |

| Economic Output | $2.4 billion | $1 billion |

| Contribution to Ohio GDP | $1 billion | $477 million |

| Jobs Multiplier (non-construction) |

2.27 | 2.86 |

| Sales Multiplier | $0.81 per $1.00 | $0.72 per $1.00 |

| Annual Peak Taxes (non-construction) |

$84 million | $62 million |

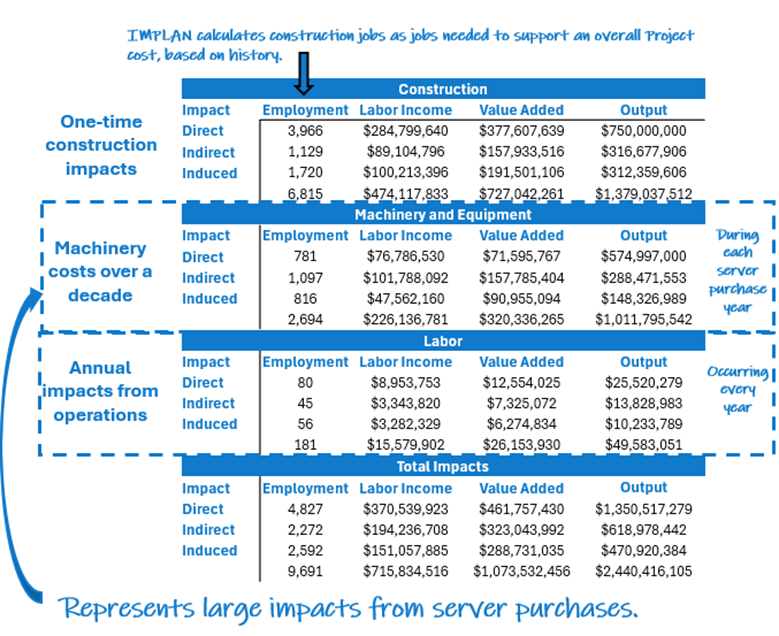

Data Center Detailed Impacts

The graphic below depicts detailed economic impacts of a data center, illustrating the time horizon each data point is subject to. This is important, as data center economic impacts represent significant spikes in economic impacts during years of large server purchases, which typically occur every 5 years. If data center economic impacts were illustrated over a 30-year time-series, a chart visualizing economic impacts would have a rollercoaster appearance.

Manufacturing Detailed Impacts

The graphic below is similar to the data center graphic above but represents the manufacturing impacts. They key takeaways are a higher degree of direct jobs and a higher job multiplier, but lower annual machinery and equipment purchases, as manufacturing machines come at a lower cost than servers, and they do not depreciate at the same rate, therefore there are longer gaps in repurchasing and the associated economic effects that result from repurchasing.

So, is one use better than the other?

The biggest conclusion that should be taken from the study results is that data centers can bring larger economic effects than the average manufacturing project. This can vary industry-to-industry within manufacturing, with some manufacturing industries having larger impacts than data centers. However, to the economic developer, choosing the data center does not come at an opportunity cost, in fact, in a typical case it can be an opportunity gain.

About the author: Chris Magill is a senior managing director for Vista Site Selection. In his role, he assists private sector clients in achieving growth through the development of site selection and economic development strategies.