Valuation Analyses

ARKANSAS' "DARK STORE THEORY" TEST CASES FOR WALMART STORES LAND IN CIRCUIT COURT

Walmart Real Estate Business Trust v. Pulaski County, et al., 60CV-19-6548 through 60CV-19-6562 (Aug. 14, 2019).

Walmart has appealed ten decisions issued by a Pulaski County judge, which rejected Walmart’s attempt to reduce a combined $145.8 million in assessed valuation to $74.3 million for tax year 2018. The independent appraisal reports that Walmart introduced as evidence for the eight Walmart and two Sam’s Club stores used all three accepted appraisal methods, but relied primarily on the sales comparison approach. The county presented no documentary appraisal evidence of their own, but criticized the selection of comparable sales, the majority of which were vacant at the time of sale, in the Walmart appraisals. After a two-day hearing, the judge ruled that Walmart’s appraisal reports were “fundamentally flawed.”

On appeal to the circuit court, Walmart argues that its values are supported by appraisal evidence utilizing the three traditional approaches to value: cost, sales, and income. They contend that their appraisal opinions assert “the real and true market value” of the properties. In a statement, a spokesperson for Walmart said that the company is “simply seeking a fair market value for the property taxation of our stores, just as any other business or homeowner should expect under state laws and constitutions that guarantee equality and uniformity for all taxpayers.”

Assessors across Arkansas view the cases as the state’s first real test of the “dark-store theory” and believe the cases will ultimately land before the Arkansas Supreme Court.

GEORGIA SUPREME COURT FINDS SECTION 42 TAX CREDITS DO NOT CONSTITUTE “ACTUAL INCOME” FOR PURPOSES OF VALUING LOW INCOME TAX CREDIT PROPERTIES

Heron Lake II Apartments, LP v. Lowndes County Board of Tax Assessors, Docket No. S19A0975 (Supreme Court of Georgia) (Sept. 23, 2019).

With the recent decision of the Supreme Court of Georgia, additional clarity has been provided to value low income housing tax credit (“LIHTC”) property. The court held that tax credits provided to investors as part of the section 42 low income housing tax credit program are not “actual income” for the purpose of an assessment and cannot be considered income when utilizing the income approach to value.

In a previous matter, decided in 2016, the Supreme Court determined that a prior statutory provision, which created a separate class of property for LIHTC properties for real estate taxation, was unconstitutional because it violated Georgia’s taxation uniformity clause. This prior decision held that the tax credits were part of the bundle of rights connected and should be taxed as real property.

After the 2016 decision, new legislation was introduced by the General Assembly that permitted either the sales comparison approach or income approach to be utilized by assessors to value a LIHTC property and further listed factors that must be considered when determining the value for LIHTC properties including: rent limitations, higher operating costs resulting from regulatory requirements, and other restrictions imposed upon the property based upon being eligible for income tax credits. The amendments also clarified that that LIHTC properties could only be considered comparable to other LIHTC properties.

In evaluating the changes to the LIHTC valuation statutes, the trial court found that tax credits were actual income for the purposes of assessment. On appeal the Supreme Court overturned that determination. The Supreme Court held that the tax credits do not provide recipients of those credits with “actual income”. Rather, when claimed by an investor the tax credits merely reduce the overall tax burden.

This is a positive decision for LIHTC properties in Georgia and endorses the use of either the sales comparison approach or income approach to value, while taking into consideration factors that may impact the value for a LIHTC property.

INDIANA TAX COURT DENIES MOTION TO DISMISS DUE PROCESS AND EQUAL PROTECTION CLAUSE CHALLENGES

Convention Headquarters Hotels, LLC v. Marion County Assessor, Indiana Tax Court, August 16, 2019, Cause No. 19T-TA-00021

The Indiana Tax Court denied an Assessor’s Motion to dismiss the claims of the taxpayer for the J.W. Marriott hotel property in in downtown Indianapolis. The taxpayer initially received a notice of increase on its partially complete hotel in 2010 raising the value of the subject property from $18,479,100 to $86,987,100. The Taxpayer filed a Notice to Initiate an Appeal with Marion County Property Tax Assessment Board of Appeals. The Board took no action to hear the matter.

In 2017, the taxpayer’s attorney’s received an email from the Assessor’s office indicating that “various properties in downtown Indianapolis were NOT assessed as partially complete.” This email caused the taxpayer to seek a Petition for Review of Assessment before the Board including, its petition that the 2010 assessment violated the equal protection and due process clauses of the U.S. Constitution. The Board did not conduct a hearing which led the taxpayer to file a direct appeal to the Indiana Tax Court. The first two appeals were remanded to the Board as the time period for the Board’s jurisdiction had not run its course.

On the third direct appeal to the Indiana Tax Court, the court assumed jurisdiction, hearing the assessor’s motion to dismiss on three issues. The court denied the assessor’s motion finding that the record was unnecessary because the matter is to be determined de novo. Second, whether the appeal was timely filed, the court recognized that the 2017 letter from the assessor was the trigger of the cause of action. The court also found that delay was caused by no fault of the taxpayer. Third, the tort claim notice was premised on the Indiana Tort Claims Act (ITCA) and it is well established that the ITCA doesn’t apply to §1983 claims. The failure to raise the issue before the Board was dealt with by the court based on its de novo jurisdiction. The matter will proceed to hearing on its merits.

KANSAS BOARD OF TAX APPEALS CUTS TAX VALUATION OF CASINO DEVELOPMENT BY MORE THAN $100 MILLION

In the Matter of the Equalization Appeal of Kansas Star Casino, L.L.C for The Year 2018 in Sumner County, Kansas, Docket Nos. 2018-2087, et al. (Aug. 12, 2019)

The Kansas Board of Tax Appeals significantly reduced the tax valuation for a gaming and entertainment development in Mulvane, KS favoring the taxpayer’s appraisal over the assessor’s. The property consists of 196 acres of land and is improved with a casino, indoor arena, conference center, and open-air event pavilion. The County’s appraised value for the entire development, which was constructed in 2012, was $180,000,000 for the 2018 tax year. The taxpayer challenged the County’s valuation for the property, arguing that it suffered from obsolescence and that 76 acres of the land was devoted to agricultural use and should be valued and classified accordingly. Prior to the hearing before the Board, the parties stipulated to an agricultural use value of $10,290 total for 63 acres, all leased as farm land, of the property’s 196 acres.

The taxpayer’s appraiser performed a cost and income approach to value the property, but he relied primarily on the cost approach. He concluded that the property’s ancillary improvements had a negative impact on the overall net income of the development. After determining that 52% of the real estate was obsolete “due to superadequacy”, he valued the property at $78,100,000 for the 2018 tax year. Meanwhile, the County’s appraiser considered all three approaches to value and also concluded that the cost approach was the most appropriate valuation methodology for the development. However, he determined that the property’s facilities were not functionally obsolete because they were “consistent with the property’s highest and best use” and “required under the management contract”. The County’s appraiser also concluded that the development did not suffer any external obsolescence. Therefore, his valuation opinion of $180,000,000 mirrored the actual construction costs for the development.

In its decision, the Board of Tax Appeals found the taxpayer’s appraisal to be the best indication of value for the property and was persuaded that there is “significant obsolescence in the development, which the County has failed to recognize.” However, the Board determined that 13 of the 76 acres that the taxpayer sought to have valued as agricultural use value was a drainage area that should be classified and valued as commercial use land. Therefore, the Board concluded that the property’s 2018 tax year valuation should be $78,913,590 rather than $78,100,000.

KANSAS BOARD OF TAX APPEALS DETERMINES THAT COST APPROACH WAS BEST INDICATOR OF VALUE FOR 6 HOME DEPOT STORES

In the Matter of the Equalization Appeals of HD Development of Maryland, Inc., Kan. Board of Tax Appeals., Docket Nos. 2016-3455-EQ, et al. (Sept. 5, 2019)

The Kansas Board of Tax Appeals recently determined that because neither an income nor a sales approach could be supported to value six Home Depot stores, the county’s cost approach was the best indicator of the stores’ market values. The Board rejected Home Depot’s sales comparison approaches, noting that all of the comparable sales had different highest and best uses, were inferior in size and location, and overall were too dissimilar to the subject properties. The Board also rejected both Home Depot and the County’s respective income approaches, pointing again to the dissimilar properties utilized by Home Depot and also pointed to the dissimilar leases the County relied upon. The Board concluded that the parties’ other proposed valuation methods were problematic because of a lack of reliable market data, and, as a result, upheld the County’s cost approach.

KANSAS BOARD OF TAX APPEALS FINDS COSTCO’S VALUE SHOULD BE REDUCED BASED UPON INCOME APPROACH TO VALUE

In the matter of the Protest of Costco Wholesale Corporation, Docket Nos. 2017-989-PR and 2017-2784-EQ (Aug. 23, 2019).

In a summary decision, the Kansas Board of Tax Appeals determined that the income approach to value based upon the Costco’s appraiser’s analysis should be utilized to value the property for tax years 2016 and 2017. The County had relied upon an income approach to value to determine the value, despite retaining an appraiser who concluded to a higher valuation. Costco relied upon the sales comparison approach to value, with additional support from the income and cost approaches. The BTA determined that the income approach to value was most appropriate, but found that Costco’s figures more accurately reflected the market finding that the County’s rental rate was too high, its vacancy rate was too low, its cap rate too low, and failed to account for taxes at vacancy. The BTA granted a reduction from the County’s original value of $17,753,000 in 2016 to $10,440,000 and from $14,927,000 to $10,840,000 in 2017.

LOUISIANA ORDERS VALUATION OF RIVERBOAT CASINO AND HOTEL USING COST APPROACH

Edmiston, Bossier Parish Assessor v. Louisiana Riverboat Gaming Partnership, et al. (Sep. 9, 2019) Louisiana Court of Appeals, Case No. 52, 948-CA.

The Court of Appeals determined that the proper method for valuing a casino and hotel was the cost approach but that the Louisiana Tax Commission (“LTC”) erred in failing to adopt the depreciation factor employed by the expert appraiser in the case.

At issue was the value of a 37 acre parcel consisting of a riverboat casino, hotel, and parking lot. For tax year 2017, the county assessor valued the property at $69,967,000. The casino owner appealed to the LTC, arguing that its expert appraisal evidence supported a value of $27,000,000. The LTC, in turn, had its staff appraiser prepare an appraisal of the property. The staff appraiser used the cost approach to determine a value of $46,932,000. This included a deprecation factor of 30%. The LTC relied on the staff appraiser’s cost approach with one change. The LTC determined that a 65% depreciation factor should be used due to the condition of the property.

On appeal, the court of appeals ruled that the cost approach was the appropriate method for valuing a casino and hotel. The court stated that the sales comparison approach was not typically used given the unique nature of a casino property and the lack of available comparable properties. The income approach also was rejected because such an approach requires significant financial data that often is not available from a casino. For these reasons, the court found that the LTC’s rejection of the owner’s expert appraisal evidence, which relied primarily on the income approach, was appropriate.

While the cost approach should be considered, the court of appeal vacated the LTC’s adoption of a 65% depreciation rate. The court acknowledged that the LTC pointed to the property’s physical condition and declining revenue for its decision, but gave no basis for the calculation of the factor. The court stated that the LTC seemed to have “plucked [the 65% factor] out of thin air.” Because the LTC’s factor lacked specific justification, the court deemed the factor to be “incorrect on its face.” On the other hand, the court found that the staff appraiser inspected the property and explained the reasons for his 30% depreciation factor. Consequently, the court remanded the matter with orders that the LTC adopt a value of $46,932,000 based upon the staff appraiser’s cost approach.

MICHIGAN TAX TRIBUNAL HOLDS THAT SALES COMPARISON APPROACH IS APPROPRIATE METHOD TO VALUE BIG-BOX RETAIL PROPERTY

Lowe’s Home Centers Inc. (#1750) v. Scio Township, Michigan Tax Tribunal, Docket No. 17-001076 (August 26, 2019)

Lowe’s filed an appeal to decrease the assessment for its owner-occupied “big-box” retail store for tax year 2016. At the Michigan Tax Tribunal, Lowe’s and Scio Township presented competing appraisals in support of their respective valuation positions. Both appraisers performed a sales comparison approach, income approach and cost approach, but each gave the approaches different or no weight in their final valuation conclusion.

The Tribunal determined that the sales comparison approach was the most relevant for determining the value for the tax year at issue. In comparing Lowe’s appraisal to the township’s appraisal, the Tribunal agreed with Lowe’s appraiser that there was an active market for the sale of big-box stores and that there was no requirement that he consider the cost approach under Menard Inc. v. City of Escanaba. The Tribunal also noted that the township’s appraisal was rife with errors, including both methodology and calculation errors that rendered the report unreliable and not competent probative evidence of value. Since the township did not produce any evidence to establish that the property owner’s appraiser’s methodology was erroneous, the Tribunal adopted the property owner’s approach.

MICHIGAN TAX TRIBUNAL INDEPENDENTLY DETERMINES VALUE OF LARGE AUTOMOTIVE INDUSTRIAL PROPERTY AFTER REJECTING COMPETING APPRAISALS

Detroit Diesel Corporation v. Redford Township, Michigan Tax Tribunal, Docket No. 17-001174 (July 11, 2019)

The Michigan Tax Tribunal reviewed the Detroit Diesel Corporation’s complaint to reduce the assessment on its 3,000,000 square foot diesel engine, transmission and axel manufacturing plant for the 2017 tax year. The subject property was occupied by a single-user manufacturer. The building had lower ceiling heights and less dock doors than most manufacturing and warehouse/distribution uses in the current marketplace.

The property owner and Redford Township each offered competing appraisals for the subject property. The Tribunal sided with the property owner’s appraiser in his assessment of the highest and best use for the subject property as industrial use, which could include single-user manufacturing or warehouse/distribution with likely conversion to a multi-tenant space. The township’s appraiser had contended that the highest and best use was for continued single-user manufacturing, but offered only one sale comparable where such a use occurred.

The Tribunal was perplexed that although both appraisers had employed the sales comparison approach, the two valuations were wildly different. The property owner’s appraiser opined to a value of $9,410,000 and the township’s appraiser opined to a value of $50,000,000. Notably neither appraisal shared a single comparable sale.

Recognizing the difficulty of the appraisal assignment, in a somewhat unorthodox effort to perform its independent valuation analysis, the Tribunal utilized only one of the sales comparables used by the property owner’s appraiser: a significantly smaller former General Motors Powertrain plant located less than 2 miles from the subject property with an electrical substation and similar environmental monitoring burdens. The Tribunal agreed only with the property owner’s appraiser’s adjustment for deferred maintenance for the roof, which resulted in an adjustment to $6.04/square foot. Ultimately, the Tribunal utilized the adjusted sale price of $6.04/square foot and multiplied it to the 3,000,000 square feet for the subject property to arrive at a final value of $15,900,000.

MICHIGAN TAX TRIBUNAL FINDS FOR PROPERTY OWNER IN APPEAL INVOLVING WALMART GROUND LEASE

Walmart Real Estate Business Trust v. Lansing Township, MTT (Docket No. 16-003180), issued July 19, 2019.

Walmart challenged the assessment of the land and improvements comprising its Lansing Township store for tax years 2016 and 2017.

The subject property was subject to a ground lease, which the township’s appraiser claimed was the basis for valuing the land separately from the building. The Michigan Tax Tribunal rejected the township’s appraiser’s disjointed highest and best use analysis because it valued the land and the improvements separately, when the land and improvements were a single economic unit. The Tribunal also criticized the township’s appraiser’s cost approach which did not account for any functional or external obsolescence to the subject property as it did not value the whole economic unit. The Tribunal also found that the township’s appraiser had failed to make any property rights adjustments in his income approach, had limited data regarding the leases he reviewed, and essentially “backed into” his land value from Walmart build-to-suit leases. The township’s appraiser did not include a sales comparison approach in his report.

In contrast, the Property Owner’s appraiser utilized all three methods to valuation to determine a final value for the subject property. Given its criticisms of the township’s appraisal report, the Tribunal found that the Walmart’s appraisal was the most reliable and credible evidence for determining the market value for the subject property.

MINNESOTA SUPREME COURT FINDS THAT THE MINNESOTA TAX COURT PARTIALLY ERRED IN VALUATION OF MALL

KCP Hastings LLC v. County of Dakota, 931 N.W.2d 773 (Minn. July 19, 2019).

The Minnesota Supreme Court ruled that the Minnesota Tax Court partially erred in its valuation of a shopping mall. The owner of the shopping mall had argued that the tax court had committed several errors in reaching its new valuation conclusion for the property following the Supreme Court’s first remand to the tax court. Although the Supreme Court rejected most of the owner’s arguments on appeal, it did find that the tax court erred by assigning value to an outlot on the property on the speculative basis that it could be sold and developed, and by using the incorrect gross building area to calculate the mall’s valuation.

The Supreme Court found that the tax court erred when it assigned value to a portion of the mall’s parking lot based on the “possibility of its sale and development”. The property owner argued that the outlot could not be sold and developed without violating the city zoning code that requires one parking space per 200 square feet of retail space. The tax court had concluded that potential buyers could seek variances from the zoning restriction. However, the higher court held that there was no evidence that the zoning code would be changed or a variance granted by the city, and that any development of the outlot would come with its own separate parking requirements. The higher court found that the “mere possibility” that the property owner and hypothetical outlot purchaser “could enter into a reciprocal easement is not ‘a reasonable probability’ that such an easement would allow the [property owner] to meet the zoning code’s requirements if it sold the outlot.”

The higher court also found that the tax court erred when it used the incorrect square footage to value the property. The tax court had used the gross building area of 153,749 square feet to value the property despite the fact that the parties had already stipulated to a different gross building area. The higher court determined that the tax court should have used the gross leasable area of 129,475 square feet, the building area arrived at in the stipulation between the parties, as the gross building area to calculate the property’s value.

Despite these findings of error, the Supreme Court found that the tax court did not (1) abuse its discretion or exceed the scope of the remand by admitting a discounted-cash-flow analysis prepared by the County, (2) did not clearly err when it found that the appraisal conducted by the taxpayer’s expert was a leased-fee appraisal, (3) did not clearly err when it rejected the vacancy rates used by taxpayer’s expert, (4) did not clearly err when it determined the terminal capitalization and discount rates based on market-survey evidence, and (5) did not abuse its discretion.

MINNESOTA TAX COURT ORDERS COUNTY TO TURN OVER FINANCIAL DATA FROM COMPETING DOWNTOWN HOTELS AS PART OF VALUATION DISPUTE

1300 Nicollet, LLC v. County of Hennepin, Minn. Tax Ct., Docket Nos. 27-CV-17-06284, et al. (Sept. 18, 2019).

The Minnesota Tax Court recently ruled on a discovery dispute involving the owner of a hotel in downtown Minneapolis and the county assessor. The owner, who was seeking a reduction in the hotel’s valuation, issued discovery to the county requesting tenancy and income and expense information that other downtown hotels had recently submitted to the assessor’s office. The county objected to the requests as overly burdensome; the other hotel owners intervened in the matter and objected to the disclosure of the information, arguing that the information was protected and that providing it to a competitor would cause substantial harm. The Court noted that while the county was opposed to disclosing the information to the requesting owner, the county had given some of the data to its own appraisers. After weighing the competing interests, the Court determined that the benefit of disclosing the data that the county had shared with its experts outweighed the confidentiality interests of the other hotel owners. As a result, the Court ordered the county to disclose any data on which its experts had relied.

MISSOURI STATE TAX COMMISSION DENIES CHARITABLE EXEMPTION TO MAJORITY OF PARCELS OWNED BY NON-PROFIT, BUT GRANTS PROSPECTIVE USE EXEMPTION ON SOME PARCELS

The Housing Partnership, Inc. v. Jake Zimmerman, Assessor, St. Louis County, Missouri, Miss. State Tax Comm., Appeal Nos. 18-11088, et al. (Sept. 20, 2019).

The Missouri State Tax Commission granted exemption for several parcels owed by a non-profit housing partnership, while denying exemption to numerous other related parcels. The partnership, which was created to develop, rehabilitate and construct affordable housing opportunities to low and moderate income individuals and families, sought exemption for 33 parcels which related to a mix of green space, vacant land, and apartments and office space. The Commission ultimately granted exemption as to 9 of the parcels, but denied exemption for the remaining 24 parcels. While the partnership claimed that it used all of the subject parcels for a charitable use, outlining both its current use and future plans for remodel and development, the Commission determined that the partnership had not shown that all parcels were “dedicated unconditionally” to charitable use. Specifically, the Commission denied exemption to the parcels that the partnership deemed green space and to those with commercial development plans, noting that neither green space nor commercial use are entitled to charitable exemption. For the remaining parcels, the Commission determined that the parcels for which the partnership had concrete development plans were entitled to exemption; but the mere discussion of developing plans in the future for the others was not sufficient.

NEBRASKA APPEALS COURT AFFIRMS BOARD OF EQUALIZATION VALUE ON WAREHOUSE PROPERTY AND REJECTS ARGUMENT THAT THE PROPERTY'S VALUE WAS NOT EQUALIZED WITH SIMILAR PROPERTIES.

Millard Lumber v. Douglas Cty. Bd. of Eqaul. (Aug. 27, 2019), Neb. Court of Appeals No. A-18-1091.

The court affirmed a Board of Equalization decision of value for a 609,633 square foot distribution warehouse. For 2017, the Douglas County Assessor determined a value for the warehouse of $13,496,200. The owner appealed, arguing for a value of $9,410,735. At hearing, the owner argued that its tax assessment was not equalized with the property adjacent to it. The owner presented evidence from a general contractor that the subject property and the adjacent property were of similar age, in similar condition, had similar traits, and used for similar purposes. However, the subject property was valued at $15.05 per square foot, while the adjacent property was valued at $8.50 per square foot. Following hearing, the assessor’s $13,496,200 was affirmed.

The Court of appeals affirmed the lower tribunal’s decision. The court agreed that Nebraska’s Constitution does require that real property be taxed “by valuation uniformly and proportionately.” An owner may challenge an assessment for the reason that the” value has not been fairly and properly equalized when considered in connection with the assessment of other property and that such disparity and lack of uniformity result in a discriminatory, unjust, and unfair assessment.” However, the burden placed on the owner is more than showing a mere difference in valuation. Rather, the owner must establish “by clear and convincing evidence that the valuation placed upon the taxpayer’s property, when compared with valuations placed on other similar properties, is grossly excessive and is the result of a systematic exercise of intentional will or failure of plain legal duty, and not mere errors of judgment.”

Here, the owner tried only to argue that the two properties were similar, which was insufficient to meet the burden established by Nebraska law. Moreover, the court agreed with the board’s determination that the two buildings were not sufficiently similar to be considered comparable and, therefore, should not have been equalized. The subject property is smaller, had a better condition rating, more area protected by fire sprinklers, more area of heavy duty concrete paving, and a more efficient heating system than the adjacent property. The subject property is classified as a distribution warehouse, while the adjacent property is classified as a storage warehouse. As such, the owner failed to prove by clear and convincing evidence that the subject property was similar to the adjacent property for equalization.

NEW JERSEY BUSINESS CAN’T CONTEST PROPERTY VALUE BECAUSE OF FAILURE OF PRIOR OWNER TO PROVIDE REQUESTED INCOME INFORMATION

Fulton Partners LLC v. City of New Brunswick, Case No. A-4886-17T2 (Superior Court of New Jersey, Appellate Division), (Oct. 11, 2019)

The Tax Court determined that the current owner could not contest the valuation of its property because the prior owner did not reply to requested income as required by statute. Fulton Partners LLC filed an appeal of the 2017 tax assessment of an income producing property it purchased from Fulton Gardens Associates, LLP on August 16, 2016 for $3,500,000. The deed was not recorded until December 21, 2016. Prior to sale, the assessor sent the prior owner, Fulton Gardens, a request for income and expense information with a due date of July 21, 2016. No response was ever received, and thus the City argued that the failure to comply with the income requested barred contesting the property’s valuation. The tax court decided not to proceed with a reasonableness hearing and held that the current owner could not pursue the reduction on appeal. The appellate court affirmed the tax court’s finding.

NORTH CAROLINA TAX COMMISSION ACCEPTS LIHTC OWNERS’ INCOME APPROACH UTILIZING ACTUAL EXPENSES; REJECTS COUNTY’S USE OF EXPENSE RATIO

In the Matter of the Appeals of Kimberly Park II, LLC, et al., from the decisions of the Forsyth County Board of Equalization and Review, Case Nos. 18 PTC 0029, et al., North Carolina Property Tax Commission (July 15, 2019).

The North Carolina Property Tax Commission recently ruled in favor of several low-income housing tax credit (LIHTC) property owners located in Raleigh, North Carolina, accepting the owners’ income approach that utilized actual expenses. While owners and the county agreed that the income approach, which is the only approved method of valuation for LIHTC properties in the state, they disagreed on the appropriate figures that should be utilized. Specifically, the parties stipulated to the capitalization and effective gross incomes, but disagreed on the appropriate measure of operating expenses to be used. The owners relied upon an income approach that utilized actual operating expense figures. The county claimed that the owners’ expenses were excessive, utilizing an operating expense, or percentage of effective gross income, in its own income approach. The county argued that its expense figure was assumed to be typical for LIHTC properties, though the county offered no evidence to support this claim. The Commission determined that because the county was unable to show that the actual figures were excessive and also could not support its own ratio, the owners’ income approach was the best indicator of the subject properties’ values.

OHIO APPEALS COURT AFFIRMS BTA’S INCREASE IN VALUE FOR A MCDONALD’S RESTAURANT

McDonalds USA L.L.C. v. Lorain Cty. Bd. of Revision, 2019-Ohio-4217 (9th District Court of Appeals) (Oct. 16, 2019)

McDonald’s appealed a decision of the BTA increasing the value of a Lorain County restaurant from $1,323,110 to $1,930,000. McDonald’s initially filed a complaint seeking a decrease in value to $715,000. At the BTA both McDonald’s and Lorain County obtained appraisals. The BTA found Lorain County’s appraisal to be the best evidence of value. On appeal from the BTA, McDonald’s advanced several arguments, but ultimately the appellate court affirmed the BTA. The court determined that the decision was reasonable and supported by evidence in the record. The Court also addressed McDonald’s allegation that the BTA had erred regarding highest and best use, finding that the BTA did not err by determining a specific highest and best use of national fast food restaurants for the subject property. The court stated that it was reasonable for the BTA to determine that it was more appropriate to use similar properties and make adjustments for locational differences, as opposed to using dissimilar properties that were closer in location to the subject property. Ultimately, the court found that McDonald’s arguments on appeal did not establish that the BTA erred in part because McDonald’s failed to cite to authority to support several of the errors it advanced.

OHIO BOARD OF TAX APPEALS CONCLUDES OWNER OCCUPIED LOWE’S HIGHEST AND BEST USE IS FOR THE CURRENT USER

Lowe’s Home Centers, LLC v. Cuyahoga Cty. Bd. of Revision, BTA No. 2017-39, (Feb. 26, 2019)

This appeal involves the valuation of an owner-occupied Lowe’s store constructed in 1999. Both the property owner and BOE obtained appraisals before the BTA. For tax year 2015, the fiscal officer originally valued the property at $9,500,000, the appraiser for Lowe’s opined to value at $6,790,000 and the BOE appraiser opined to value at $12,020,000.

The BTA began its analysis of the two appraisals by reviewing the appraisers’ determination of the property’s highest and best use. The appraiser for Lowe’s determined that it was for the “continued use as a single tenant retail facility…” and noted that the improvements were functionally obsolete for most second generation users due to the substantial amount of accrued depreciation. The BOE appraiser determined that the highest and best use was “for continued use by the current occupant for its ongoing business” explaining that the improvements continue to make a substantial contribution to the property’s overall value. The appraiser for Lowe’s focused on sales and leases of properties no longer occupied by its original intended user, and the BOE appraiser focused on properties that continue to be occupied by its original intended user.

The BTA determined that there was no evidence of Lowe’s vacating properties of similar age and determined that the BOE’s highest and best use was most appropriate. It further stated that it found the “special purpose” doctrine to be applicable and that consideration of first generation comparables, comparables occupied by the original intended user, were the most appropriate. The BTA disregarded the arguments by Lowe’s regarding making property rights adjustments to the owner-occupied property, but determined that proper adjustments were considered. The BTA found that the BOE’s value of $12,020,000 was the best indication of value for tax year 2015.

OHIO BOARD OF TAX APPEALS FURTHER CONFIRMS METHOD FOR DETERMINING VALUE FOR SKILLED NURSING FACILITY

Marietta Care, L.L.C. v. Washington Cty. Bd. of Revision, et al., BTA 2017-1723 (Sept. 5, 2019).

The owner of a 150-bed skilled nursing facility built in 1985 filed a complaint with the Washington County Board of Revision to reduce the facility’s assessment. The owner submitted an appraisal report utilizing a sales comparison approach and an income approach, which arrived at a value of $3,000,000 for tax year 2016. The BOR issued a decision retaining the original assessment for the property and the property owner appealed the case to the Ohio Board of Tax Appeals.

At the BTA, the county submitted a competing appraisal report containing an income and sales comparison approach, which indicated a value of $6,110,000. The BTA reviewed both appraisal reports and focused almost exclusively on the correct application of the income approach to value.

The BTA criticized the county’s appraisal report because it failed to comport with the requirements for conducting an income approach set forth in a recent Supreme Court decision. Specifically, the BTA noted that the county’s appraiser utilized a lease-coverage ratio under the income approach to value and that the leases reflected business value, not realty value. The BTA also criticized owner’s appraisal report because appraiser’s utilized the subject property’s actual expense data, which was not supported by any market data.

In its independent calculation of value, the BTA utilized the property owner’s appraiser’s income approach and going concern value, but relied upon the county appraiser’s expense data, to arrive at a value for the subject property for tax year 2016.

OHIO BOARD OF TAX APPEALS REJECTS APPRAISAL OF LIHTC PROPERTY THAT RELIED UPON CONVENTIONAL HOUSING MARKET RENTS

Forest Edge LLC v. Hancock County Bd. of Revision, BTA No. 2017-1370 (Sept. 11, 2019).

In a recent case of competing appraisals involving a low-income housing tax credit (LIHTC) property, the Ohio Board of Tax Appeals sided with the owner, confirming that an appraiser must take LIHTC restrictions into account. Both of the appraisers solely developed income approaches to value, but utilized different methods to determine a market rent. The owner’s appraiser relied upon comparable LIHTC properties to determine a LIHTC market rent. Conversely, the county’s appraiser relied upon conventional, market rate single-family homes to determine a conventional market rent. The Board concluded that the owner’s appraiser provided the best estimate of the subject property’s value because he considered the restrictive covenant and relied upon the LIHTC market for his analysis. Because the county’s appraiser did not consider the restrictive covenant and relied upon the conventional housing market in his analysis, his report did not satisfy the requirement that LIHTC restrictions be considered.

OREGON SUPREME COURT UPHOLDS REDUCTION FOR HIGH VACANCY SHOPPING CENTER

Powell Street I, LLC v. Multnomah County Assessor, Case No. S065290, (July 25, 2019).

The Oregon Supreme Court affirmed the Tax Court’s decision, which concluded a reduction was warranted for a shopping center that had more than 50% vacancy and no anchor tenant. The state argued that the property should be valued as stabilized. For January 1, 2014 the assessor originally valued the property at $14.7 million. Both the shopping center and the assessor obtained appraisals. The shopping center’s appraiser concluded to a value of $10.13 and the assessor’s appraiser concluded to a value of $17.5. The tax court accepted the taxpayer’s appraisal finding the stabilization deduction to account for the substantial vacancy and missing anchor appropriate.

On appeal, the state argued that vacancy and missing anchor were characteristics of the owner and not the property. The Supreme Court found that the facts in the record disputed this argument (exposure period for vacant anchor space) and further found that evidence in the record supported the tax court’s determination. The Court also determined that a buyer of the property would take into account the vacancy and missing anchor and therefore it was appropriate to take those factors into consideration.

PENNSYLVANIA COMMONWEALTH COURT RULES THAT SCHOOL DISTRICT'S DECISION TO APPEAL ONLY THE ASSESSMENTS OF COMMERCIAL PROPERTY IS AN UNCONSTITUTIONAL EXERCISE OF THE DISTRICT'S DISCRETION

The School District of Philadelphia v. Bd. of Revision of Taxes (Aug. 22, 2019), Commonwealth Court No. 1493 C.D. 2017, et. al.

The Pennsylvania Commonwealth Court considered a claim by various commercial property owners that the school district was filing appeals contesting property assessments on commercial properties only, while at the same time not contesting the values of potentially under-assessed residential properties. The owners claimed that the practice violated the uniformity clause of the Commonwealth’s constitution.

The Uniformity Clause of the Pennsylvania Constitution provides that “[a]ll taxes shall be uniform, upon the same class of subjects, within the territorial limits of the authority levying the tax, and shall be levied and collected under general laws.” Pa. Const. art. VIII, § 1. Relying on a prior decision in Valley Forge, the court concluded that, within a taxing district all real property “is a single class.” For this reason, “the Uniformity Clause does not permit the government, including taxing authorities, to treat different property sub-classifications in a disparate manner.” Id. In Valley Forge, commercial property owners challenged the school district's policy of appealing their tax assessments while ignoring under-assessed, single-family homes within the school district. The Pennsylvania Supreme Court ruled that a policy to appeal only the assessments of one classification of properties, is an unconstitutional exercise of the authority's discretion. The Supreme Court further explained that systematic pursuit of the tax laws based on property type, even absent wrongful conduct, is constitutionally prohibited.

In this case, while the court agreed that a policy of appealing commercial properties only could violate uniformity provisions, there has been no evidentiary hearing to establish the facts. Thus, the matter was remanded so that the lower court could make a findings of facts as to the district’s selection process for assessment appeals.

SOUTH CAROLINA SUPREME COURT RELIES ON ABSURDITY PRINCIPLE TO DENY HAMPTON INN’S ATTEMPT TO VALUE HOTEL AS VACANT LOT

Charles County Assessor v. University Ventures, LLC, South Carolina Supreme Court, Opinion No. 27907 (July 24, 2019).

The South Carolina Supreme Court recently rejected Hampton Inn’s attempt to value one of its hotels based on the property’s status prior to construction. The Court noted that to do so would violate the absurdity principle, which requires a court, when interpreting a statute, to avoid an interpretation that leads to an absurd consequence. The principle is based on the notion that the legislators could not have intended to create absurdity in the law.

The subject property was considered vacant and valued accordingly for tax years 2008 and 2009 while it was still under construction. Construction was completed in April of 2009 and the Assessor valued the property at $8.18 million for tax year 2010. The owner did not contest the tax year 2010 value, but did file an appeal relating to tax year 2011, arguing that the statutory timeline mandating reassessments every fourth year required that the property be valued based on its status in 2008, when it was a vacant a lot.

In a factually confusing case, the Court ultimately decided that it would be absurd to allow the improvements to go on the assessment rolls for tax year 2010 and then value the property as vacant for 2011.

TENNESSEE STATE BOARD OF EQUALIZATION RETAINS LOCAL COUNTY BOARD’S VALUATION FOR RETAIL BANK BRANCH

In re: Memphis Bank & Trust Company, Tenn. SBE Dkt. No. 113320, (October 10, 2019).

The Tennessee State Board of Equalization upheld the Shelby County Board of Equalization’s 2017 tax year valuation for a 10,600 square foot retail bank branch in Memphis. The taxpayer’s appraisal witness valued the bank under the sales comparison and income capitalization approaches and opined to a value of $800,000. None of the comparable sales provided by the taxpayer’s appraiser were from the same area as the subject property. Despite the fact that the comparables sales were located in other locations, he made the exact same location adjustment to each comparable sale. Moreover, the taxpayer’s appraiser utilized non-bank retail leases to support his market rental rate in his income capitalization approach.

Meanwhile, the County’s staff appraiser analyzed the property under all thee valuation approaches but primarily relied on a cost approach to value the bank at $2,174,300. Although the bank was built in 1954, it was his opinion that the cost approach would best identify the fair market value of the property. He believed that the property did not suffer any functional obsolescence since it was continuing to be used as a bank.

After evaluating the appraisals and witness testimony supplied by the taxpayer and County, the administrative law judge was not persuaded by the taxpayer’s valuation analysis and upheld the County Board of Equalization’s valuation of $1,711,400 for the bank. In her holding, the judge indicated that the property still operates as a bank despite its age and Assessor’s cost approach supports the value established by the local board. Additionally, the judge concluded that the vacant land sales cited by the Assessor were recent, geographically relevant and properly adjusted.

TENNESSEE BOARD OF EQUALIZATION FINDS THAT PROPERTY USED TO DISTILL WHISKEY SHOULD BE VALUED AS COMMERCIAL PROPERTY, NOT AS AGRICULTURAL PROPERTY.

In re: Samuel P. Bryant, Taxpayer, Tenn. Bd. of Equalization No. 111929 (Aug. 6, 2019).

The Tennessee Board of Equalization recently reclassified property used to distill whiskey as commercial, rather than agricultural. In the case, the owner built a pole barn and distillery on formerly agricultural land. The owner claimed that the land should continue to be taxed as agricultural land because the distillation of grains into liquor is an agricultural process in and of itself, and that the yeast used in the process should be considered the owner’s “livestock,” just like cows, pigs, or any other animal. The Board rejected the argument, finding that “distilling is not traditionally considered an agricultural use of property, especially not when combined with a tasting room and store.”

The owner also argued that the pole barn and distillery should be exempt from real property tax because they were made from locally sourced trees. Tennessee law holds that “no article manufactured of the produce of Tennessee shall be taxed other than to pay inspection fees.” However, the Board ruled that this exemption does not apply to real property tax on buildings erected from resources found in the state.

TENNESSEE STATE BOARD RETAINS LOCAL BOARD’S VALUATION FOR VACANT BIG BOX RETAIL STORE BASED UPON LAND VALUES

In re: Harton Family Partners, Tenn. SBE Dkt. No 119900, (October 16, 2019).

The Tennessee State Board of Equalization has upheld the Coffee County Board of Equalization’s 2018 tax year valuation for a former K-mart property. The taxpayer had contended that the property should be valued at no more than $1,050,000 based upon the original purchase price of the property, recent sale offers for the property, a sale listing of K-Mart in another state, and the decline of big-box retail. The taxpayer also argued that a willing and informed buyer would perceive the long-term ground lease on the property as an encumbrance that would substantially reduce the value of the land. The County supported its valuation by presenting five land sales and a listing of commercial land tracts within the immediate area of the subject property. The Assessor’s land valuation presentation opinion of $2,200,000 exceeded the county board’s determination of $2,027,000. In affirming the county board’s determination of value, the administrative law judge stated “the gap between the assessor’s $2,200,000 raw land valuation and the $2,027,000 County board determination on the total value of the subject would seem to reasonably accommodate any perceived detrimental effect the improvements may have actually had on the value of the subject.” Moreover, the judge questioned whether or not the highest and best use of the property still remained as single tenant “large-scale” retail.

WASHINGTON BOARD OF TAX APPEALS REDUCES VALUATION OF OFFICE BUILDINGS BASED ON EVIDENCE THAT VACANCY HAD NEGATIVE IMPACT ON PROPERTY’S MARKET VALUE

John Wilson v. East Campus 3, Washington Bd. of Tax Appeals, Docket Nos. 91505 & 91506 (May 10, 2019).

The Washington Board of Tax Appeals determined that the occupancy status of two single-tenant office buildings negatively impacted the value of those building and upheld the reduction in the assessment as determined by the King County Board of Equalization.

In assessment year 2015, the property owner appealed the assessments for two office buildings located in the Federal Way area. The property owner asserted that the assessor failed to take into account the properties’ vacancy issues in establishing the assessments. The property owner presented an appraisal report at the County Board which confirmed that both office buildings were single-tenant properties that were 100% vacant on the assessment date. The property owner had been unsuccessful in attracting another single tenant to lease the properties for nearly three years. The appraisal reports indicated that the buildings would likely need to be converted for use as multi-tenant buildings before they could be leased. The property owner’s appraiser conducted both an income approach and a sales comparison approach, which included four other sales of high-vacancy buildings in the same area. The Assessor for King County (“Assessor”) also submitted sales to support its request.

The Board relied upon the sales comparison approach to value and placed weight on sales from the property owner’s appraisal and the Assessor’s information. The Board noted that the sales reviewed demonstrated that the market values for vacant properties were at the lower end of the range of those sales. On that record, the Board upheld the County Board’s determination that the Assessor overvalued the subject properties for assessment year 2015.

WASHINGTON BOARD OF TAX APPEALS UPHOLDS ASSESSOR’S VALUATION FOR SUPERMARKET

Safeway v. Hjelle, BTA Docket No. 89790 (2019).

The Washington Board of Tax Appeals recently sustained the Snohomish County Board of Equalization’s decision to uphold the County’s 2014 tax assessment for a supermarket. The taxpayer contended that the 48,000 square foot supermarket should be valued at $5,207,993 rather than the Assessor’s value of $6,271,000. In support of its value opinion, the taxpayer supplied six comparable sales of retail properties in Washington that occurred between April of 2010 and April of 2015. The comparables supplied by the taxpayer were located in various parts of Washington. The taxpayer’s adjusted comparable sales ranged from $82 per square foot to $134 per square foot. The taxpayer did not perform an income approach to value the property.

The Assessor supported its valuation with four comparable sales of grocery supermarkets in Snohomish County. The assessor’s adjusted comparable sales ranged from $143 per square foot to $388 per square foot and it argued that the sales alone support the subject’s $151 per square foot assessed value. The assessor also performed an income approach that valued the property in excess of the assessor’s original tax assessment.

In its critique of the taxpayer’s valuation analysis, the Board noted that none of the taxpayer’s sale comparables were located in the County and noted that some were located in a completely different part of the state. The Board also mentioned that three of the taxpayer’s comparables occurred years before the assessment date, and that three were vacant at the time of sale. The Board, however, also criticized the wide range in sale prices in the assessor’s comparables and concluded that it could not find a significant number of comparable sales to use to value the property on the assessment date. Therefore, the Board relied upon the Assessor’s income approach as the “dominant factor in valuation” to prove that the original assessment did not exceed fair market value. The Board concluded that the property owner did not provide “clear, cogent and convincing evidence” to overcome the presumption that the assessor’s value was correct.

WASHINGTON STATE BOARD OF TAX APPEALS UPHOLDS ASSESSOR’S VALUATION FOR SEATTLE APARTMENT COMPLEX

Washington State BTA denies appeal filed by one of the nation’s largest apartment owners after relying on the income approach value conclusion determined by the County for a Seattle apartment complex.

Equity Residential vs. Wilson, BTA Docket Nos. 91654 to 91657 (May 2, 2019).

The Washington State Board of Tax Appeals recently sustained the King County Board of Equalization’s decision to uphold the original 2015 tax assessment for a Seattle apartment complex. The taxpayer had challenged the County Assessor’s $26,643,000 assessment for the subject property, a 78-unit apartment complex built in 2000 that also contains 14,000 square feet of retail space. The taxpayer relied primarily on an income approach to value the property but it also supplied four comparable sales of apartment complexes in Seattle that sold within five years of the assessment date. Under its income approach, the taxpayer applied a capitalization rate of 5.75% to its market net operating income conclusion for the residential portion of the property and then added its value opinion for the retail portion. The taxpayer’s capitalization rate conclusion was derived from the four comparable sales it proffered.

The Assessor supported its valuation with an income approach and eight comparable sales of apartment complexes, six of which sold within one year of the assessment date. The Assessor’s net operating income calculation, which incorporated both the residential and retail spaces, was nearly identical to the taxpayer’s net operating income conclusion with the exception that they utilized a capitalization rate of 5.0% rather than 5.75%. The Assessor’s capitalization rate conclusion was derived from multiple sources, including an apartment investment report for properties in King County, sixteen additional comparable sales in the subject’s neighborhood, and a CBRE report for capitalization rates for urban apartment complex sales in Seattle.

In its decision, the Board relied upon the income approach as “the dominant factor in valuation” because the sales utilized were not sufficiently similar to the subject property. The Board found that the respective net operating income estimates reached by the parties in their income approaches were very similar and that the values derived were attributable to the different capitalization rates utilized. After weighing the evidence from both parties, the Board concluded that the evidence in the record supported a capitalization rate of 5.0%, or lower, on the assessment date. The Board noted that the owner’s analysis based upon a change in capitalization rate would exceed the original assessed value. As a result, the Board found that the property owner did not provide “clear, cogent and convincing evidence” to overcome the presumption of correctness for the Assessor’s valuation.

WASHINGTON DECISION REMINDS OWNERS THAT SALES COMPARABLES MUST BE COMPARABLE

Prologis USLV vs. Wilson, BTA Docket No. 92305 (unpublished)

The Washington Board of Tax Appeals recently reiterated the necessity of carefully selecting sales utilized in the sales comparison approach that have multiple points of comparison with the subject. The Board considered the value of a property comprised of several warehouses and a small office building. The warehouses ranged in size from 33,600 square feet to 90,780 square feet, with a total area of 313,927 square feet across six buildings.

In Washington, an appraiser is required to consider a property’s highest and best use. Typically, value is derived using the sales approach; however, consideration is made for the income and cost approaches when there are insufficient sales or the property is complex. In order to prevail, a property owner must present “clear, cogent, and convincing evidence of an assessor’s error in order to prevail.”

Here, the property owner relied on three warehouse sales to challenge the assessor’s value for the subject property. The Board found that the selection of sales, while all were warehouse properties, had few other points of comparison with the subject. The sales were different in construction, vacancy and condition. In its decision, the Board noted that when relying upon sales in a competitive market, it is critical to identify and present as many points of comparison as possible with the property at issue. Because the Board found that the owner failed to present appropriate sales, the owner was unsuccessful in establishing a reduction in value.

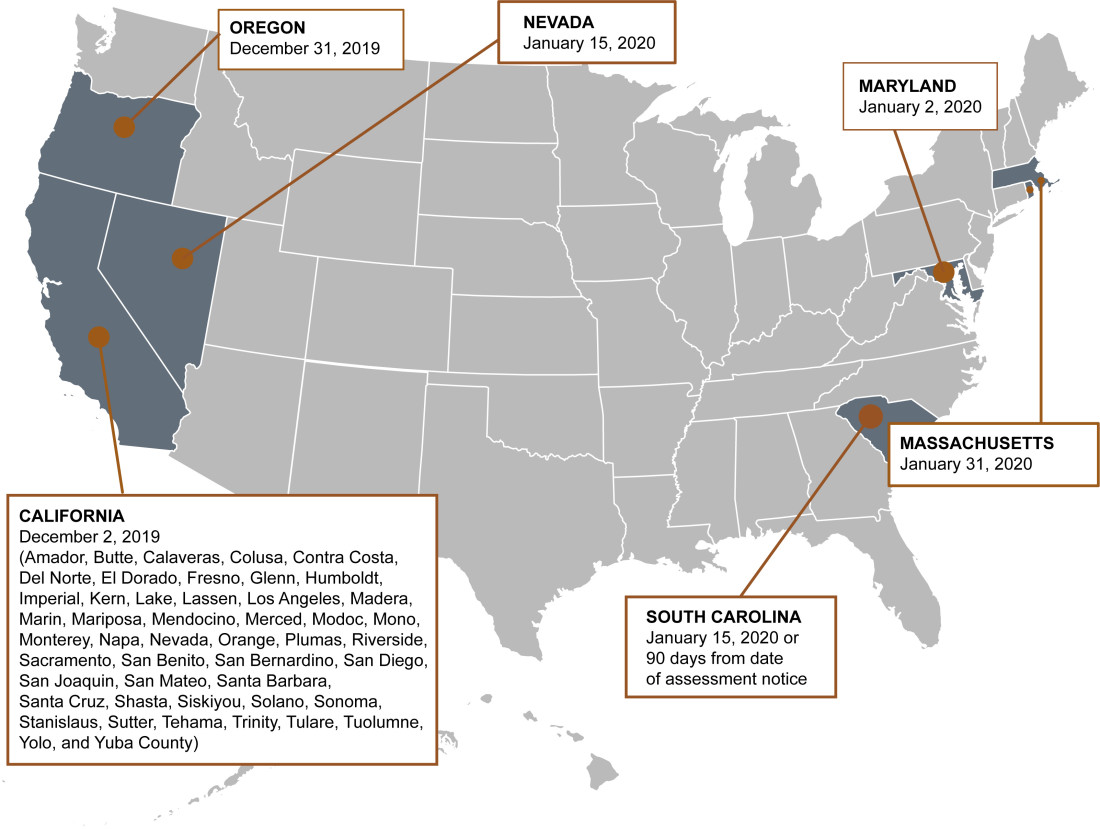

Deadlines Looming in 6 States